Executive Summary (For Financially Literate Indian Households)

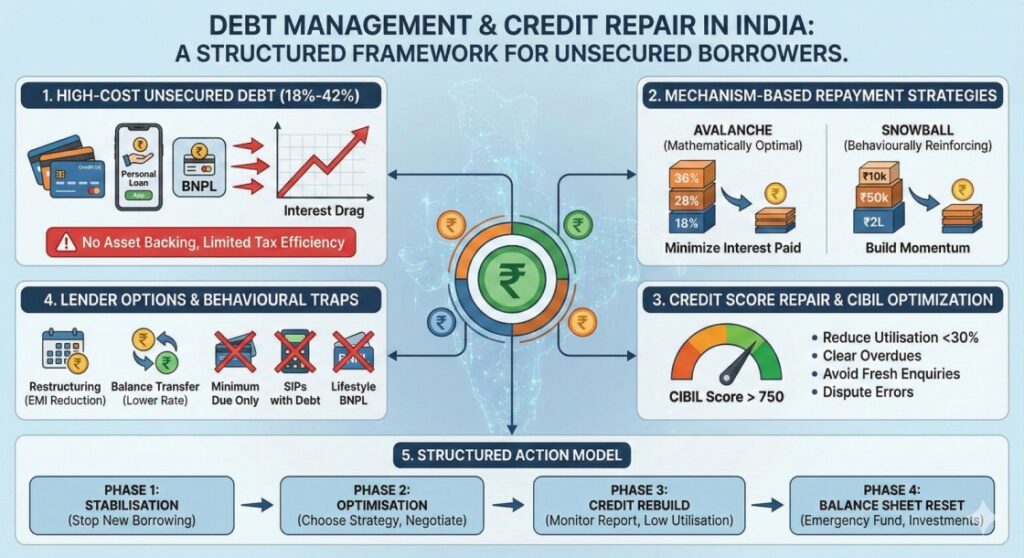

Unsecured retail debt in India—primarily credit cards, personal loans, consumer durable loans, and BNPL products—carries some of the highest interest rates in the financial system, often ranging between 18%–42% annually. Unlike home loans, these liabilities offer no asset backing, limited tax efficiency, and high compounding risk. In a rising consumption economy with easy digital credit access, many salaried and self-employed Indians accumulate fragmented debt without a structured repayment strategy.

1. Understanding Unsecured Retail Debt in the Indian Context

What qualifies as unsecured retail debt?

- Credit cards

- Personal loans

- Consumer durable loans

- BNPL (Buy Now Pay Later) products

- App-based instant loans (RBI-regulated NBFCs only)

These instruments are high-risk for lenders because they lack collateral. That risk is priced through high interest rates and penalty structures.

Structural Features

| Characteristic | Credit Cards | Personal Loans | BNPL |

| Interest Rate | 30–42% (annualised) | 14–28% | Often “0%” but embedded cost |

| Compounding | Monthly | Monthly | Depends on structure |

| Prepayment | Flexible | Often allowed | Limited flexibility |

| Credit Score Impact | High | High | Increasingly reported |

The key financial reality:

If your post-tax investment return expectation is 10–12% and your debt costs 24–36%, debt repayment is mathematically superior to investing.

This is a capital allocation decision—not an emotional one.

2. Mechanism-Based Debt Repayment Framework

Step 1: Calculate Effective Cost of Debt

Most borrowers underestimate cost because they focus on EMI, not IRR (Internal Rate of Return equivalent).

If you pay:

- ₹5 lakh credit card balance

- 36% annual rate

- Only minimum due (5%)

The interest component can exceed principal repayment for years.

Effective debt cost = Contractual interest + GST on interest + Late penalties (if any)

GST (18%) applies to interest charges and penalties, increasing the real burden.

Step 2: Choose a Repayment Strategy

1. Debt Avalanche (Mathematically Optimal)

Repay highest interest loan first.

- Minimises total interest paid

- Best for financially disciplined individuals

- Optimal for salaried professionals with stable cash flow

2. Debt Snowball (Behaviourally Reinforcing)

Repay smallest loan first.

- Creates psychological momentum

- Reduces mental load

- Suitable for borrowers juggling multiple small BNPL and card debts

Comparative Analysis

| Strategy | Interest Saved | Psychological Benefit | Suitable For |

| Avalanche | Highest | Moderate | Analytical borrowers |

| Snowball | Moderate | High | Behaviour-driven households |

For financially literate Indian borrowers, avalanche is usually superior unless behaviour is the binding constraint.

3. Cash Flow Reallocation Model (Salaried vs Self-Employed)

Salaried Professionals

Predictable monthly income allows:

- EMI stacking

- Structured prepayments

- Bonus allocation toward principal

Practical Allocation Rule

- Maintain 1 month expenses buffer

- Divert all surplus to highest-cost debt

- Pause equity SIPs if debt >18% interest

Pausing SIPs is not market timing—it is interest arbitrage.

Self-Employed Individuals

Income volatility introduces liquidity risk.

Framework:

- Build 3-month expense buffer before aggressive prepayment

- Negotiate restructuring if cash flows fluctuate

- Avoid converting working capital needs into personal credit card debt

For self-employed borrowers, liquidity risk may outweigh interest optimisation in early stages.

4. Mainstream Retail Credit Repair in India

Credit scores in India are tracked by:

- TransUnion CIBIL

- Experian India

- Equifax India

- CRIF High Mark

Most lenders prioritise CIBIL.

Credit Score Components

| Factor | Approx Weight |

| Payment History | High |

| Credit Utilisation | High |

| Credit Mix | Moderate |

| Enquiries | Moderate |

| Account Age | Low–Moderate |

Repair Mechanics

- Clear overdue accounts first

- Reduce utilisation below 30%

- Avoid fresh credit enquiries

- Convert overdue accounts to “Closed” status

- Raise dispute if incorrect reporting

Dispute channels:

- Direct bureau portal

- Lender nodal officer

- RBI CMS portal (if unresolved)

Credit repair is time-based. There is no legal “quick fix”.

5. Restructuring & Negotiation (Mainstream Retail Methods)

Options available through banks/NBFCs:

- Temporary EMI reduction

- Tenure extension

- Settlement (last resort)

- Balance transfer to lower-rate personal loan

Settlement Warning

Settlements may reduce principal but severely damage credit score for years.

Use only when:

- Severe financial distress

- No near-term borrowing need

6. Taxation Implications (India-Specific)

Unsecured personal loan interest:

- Not tax deductible (unless used for business or income-generating purposes)

If personal loan funds are used for:

- Business → Interest deductible under Income Tax Act (business expense)

- Investment in property → Interest may qualify under relevant sections (subject to conditions)

Credit card interest is generally not deductible for personal consumption.

Thus, unsecured debt is typically post-tax cost, making it even more expensive relative to investment returns.

7. Risk Analysis

1. Compounding Risk

High rates + revolving credit create exponential growth in liability.

2. Liquidity Trap

High EMIs reduce emergency fund creation, increasing dependency on more credit.

3. Credit Lockout Risk

Low score restricts access to:

- Home loans

- Business loans

- Competitive rates

4. Behavioural Risk

Digital credit apps reduce friction in borrowing.

8. Common Behavioural Mistakes Among Indian Borrowers

- Paying minimum due on credit cards

- Maintaining SIPs while revolving 30%+ credit card debt

- Taking personal loans to invest in equity markets

- Ignoring credit report errors

- Using BNPL for lifestyle consumption

Financial discipline is not about austerity—it is about cost hierarchy awareness.

9. Comparative Framework: Instruments & Their Impact

| Instrument | Expected Return Range | Risk Level | Liquidity | Tax Treatment (India) | Suitable For |

| Credit Card Debt | -30% to -42% (cost) | Very High | Revolving | No deduction | Avoid long-term |

| Personal Loan | -14% to -28% (cost) | High | EMI-bound | Usually no deduction | Short-term need |

| Liquid Fund | 4–7% | Low | High | Debt taxation | Emergency corpus |

| Equity Mutual Fund | 10–14% (long-term est.) | High | Moderate | LTCG/STCG rules apply | Long-term goals |

Debt repayment at 30% is equivalent to earning a risk-free 30% return.

10. Structured Action Framework (Non-Prescriptive)

Phase 1: Stabilisation

- Stop new borrowing

- Track full liability list

- Ensure minimum dues are covered

Phase 2: Optimisation

- Choose avalanche/snowball

- Negotiate lower interest

- Consider balance transfer

Phase 3: Credit Rebuild

- Reduce utilisation <30%

- Avoid enquiries for 6–9 months

- Monitor credit report quarterly

Phase 4: Balance Sheet Reset

- Build 3–6 month emergency fund

- Restart long-term investments

- Maintain debt-to-income <30%

Strategic Conclusion

Unsecured retail debt is a high-cost liability class within the Indian financial system. Unlike secured debt, it offers no asset backing, no meaningful tax shield, and limited structural flexibility. The correct analytical approach is capital reallocation: eliminate high-cost liabilities before pursuing nominal return assets.

For salaried individuals, the solution lies in disciplined surplus deployment. For self-employed borrowers, liquidity buffering must precede aggressive prepayment. Credit repair is not cosmetic—it is a gradual restoration of lender trust via repayment behaviour and utilisation control.

In an economy where digital credit access is frictionless, structured debt management becomes a core financial competency. The financially literate borrower does not merely repay debt—they optimise the liability side of their balance sheet with the same rigour applied to investments.