(And Why Most People Don’t Really Understand It)

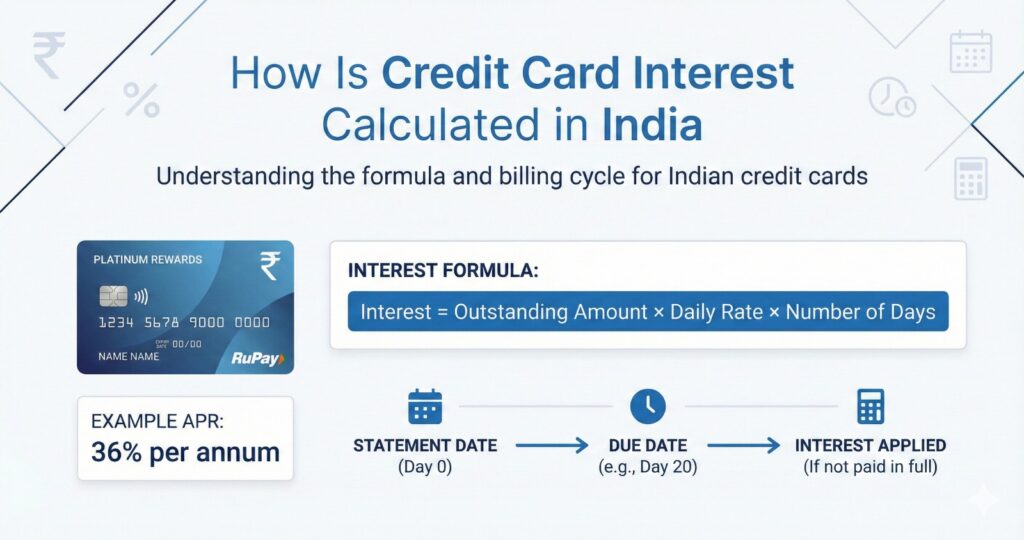

Credit card interest in India is calculated using the Average Daily Balance (ADB) method.

Banks take your Annual Percentage Rate (APR), divide it by 365, and apply that daily rate to your outstanding balance — every single day.

If you don’t pay the full statement amount by the due date:

- Interest is charged daily

- It compounds

- 18% GST is added on interest and penalties

Most Indian banks charge 30%–45% APR.

That makes revolving credit card debt one of the most expensive forms of retail borrowing in India.

💳Why Understanding Credit Card Interest in 2026 Is Non-Negotiable

Credit cards are everywhere now.

- Instant approvals

- UPI-linked RuPay credit cards

- One-click EMI conversions

- BNPL integrations

Access has become easy.

Understanding has not.

Here’s the reality:

Interest is calculated daily.

It compounds if unpaid.

And 18% GST is added on top.

Most banks charge 30%–48% APR.

If you are between 22–40 and actively using a credit card, this is not optional knowledge.

This is financial survival knowledge.

What Is Credit Card APR in India?

APR = Annual Percentage Rate

It is the yearly cost of borrowing on your credit card.

Typical Indian structure:

- Monthly interest: 2.5%–3.75%

- Annualized APR: 30%–45%+

- Cash withdrawal: Higher than purchase APR

Now understand this clearly.

If your APR is 36%, it does not mean simple 3% monthly interest.

It means:

36% ÷ 365 = 0.0986% per day

This is called the Daily Periodic Rate.

Interest is calculated every single day on your outstanding balance.

Not monthly.

Daily.

How Credit Card Interest Is Calculated (Step-by-Step)

Most Indian banks use the Average Daily Balance (ADB) method.

Step 1 — Calculate Daily Rate

If APR = 36%

Daily Rate = 36% ÷ 365

= 0.0986% per day

Step 2 — Track Daily Outstanding

Your bank tracks your balance every single day of the billing cycle.

Spend more → daily base increases.

Pay partially → daily base reduces.

Step 3 — Apply Formula

Interest =

Average Daily Balance × Daily Rate × Number of Days

That’s the engine behind the compounding.

If You Pay Full Statement Amount

- No interest on retail purchases

- 20–50 days interest-free period applies

That’s disciplined usage.

If You Pay Only Minimum Due

- Interest applies on remaining balance

- New purchases lose interest-free period

- Interest compounds daily

That’s where debt quietly accelerates.

Real Example: ₹1,00,000 Outstanding (With GST Impact)

Assumptions

- Outstanding: ₹1,00,000

- APR: 36% (~3% monthly)

- Minimum due: 5% (₹5,000)

- GST: 18% on interest

Scenario A — Full Payment

You pay ₹1,00,000.

Interest = ₹0

GST = ₹0

Total borrowing cost = ₹0

Perfect usage.

Scenario B — Minimum Due Only

You pay ₹5,000.

Remaining balance = ₹95,000.

Interest (3%) = ₹2,850

GST (18% of ₹2,850) = ₹513

Total finance charge = ₹3,363

New outstanding next month = ₹98,363.

You paid ₹5,000.

But your debt barely moved.

Continue this pattern for months and repayment can cross ₹1.2–1.3 lakh on a ₹1 lakh spend.

This is revolving debt.

What Happens to New Purchases When You Revolve?

Once you carry forward balance:

- Interest-free period disappears

- New purchases attract interest immediately

- Compounding base increases

That’s why people say:

“I keep paying every month, but balance doesn’t reduce.”

It’s not a scam.

It’s math.

Daily compounding math.

GST on Credit Card Charges in India

18% GST applies on:

- Interest charges

- Late payment fees

- Over-limit penalties

- EMI processing charges

For salaried individuals → not tax deductible.

For business users → depends on usage and GST classification.

Credit Card vs Personal Loan — Which Is Cheaper?

| Borrowing Option | Interest Rate | Best For |

| Credit Card (Revolving) | 30%–45% APR | Very short-term liquidity |

| Personal Loan | 10%–18% | Structured repayment |

| Overdraft | 9%–20% | Business cash flow |

| BNPL | 0% (on time), 24%+ if delayed | Short tenure purchases |

Credit card revolving debt is usually 2–3 times more expensive than a personal loan.

If you cannot pay your full bill, replacing high-interest revolving debt with lower-cost structured debt can be financially rational.

Why Minimum Due Is Dangerous

Minimum due exists to:

- Prevent default

- Avoid late fee

It does not:

- Stop interest

- Stop compounding

- Reduce principal meaningfully

Minimum due protects the bank.

Not your wealth.

Impact on Your CIBIL Score

Revolving balance can:

- Increase credit utilization ratio

- Reduce score if usage exceeds 30%

- Signal financial stress

Best practice:

Keep utilization below 30% of total limit.

Limit = ₹1,00,000

Ideal usage = Below ₹30,000

Discipline improves credit profile.

Behavioral Mistakes (Age 22–40)

Treating credit limit as income

Converting everything into EMI

Revolving during job instability

Checking minimum due instead of total outstanding

These are behavioral issues, not income issues.

Debt vs Investment Reality Check

If:

- Mutual fund return = 12%

- Credit card APR = 36%

You are losing 24% spread.

Paying off credit card debt gives a guaranteed 36% effective return.

No safe investment can legally promise that.

When high-interest debt exists, repayment > investing.

How to Avoid High Credit Card Interest in 2026

Pay full statement amount

Enable auto-debit

Track billing cycle

Stop spending if full payment isn’t possible

Compare personal loan vs revolving cost

Keep utilization under 30%

Avoid ATM cash withdrawals

Simple discipline. Massive difference.

Final Perspective

Credit cards in India are:

Excellent payment instruments.

Extremely expensive financing tools.

Interest is calculated:

Daily.

Compounded.

Taxed at 18% GST.

When controlled, they build credit history.

When ignored, they build debt. Control the compounding — before it controls you

Frequently Asked Question

Is credit card interest calculated daily in India?

Yes. Banks use the Average Daily Balance method, where the APR is divided by 365 and applied to the daily outstanding balance.

Does GST apply on credit card interest?

Yes. An 18% GST is applied on interest charges, late payment fees, and other finance-related charges.

What happens if I pay only the minimum due?

Interest is charged on the remaining balance, and new purchases lose the interest-free period. Debt can grow due to compounding.

Is credit card interest tax deductible?

For salaried individuals, no. For business owners, it may be deductible if classified as business expense.