In 2026, managing money smartly is not a luxury — it’s a necessity.

With rising inflation, lifestyle expenses, and uncertain income sources, personal finance has become the #1 concern for Indian households. Whether you earn ₹15,000 or ₹1,50,000 per month, learning how to budget, save, invest, and use digital tools wisely can completely change your financial future.

Why Personal Finance Is So Important in 2026

In today’s India:

- Prices of groceries, fuel, rent, and education are rising 📈

- Job security is not guaranteed

- Medical and emergency costs can come anytime

That’s why managing money wisely is more important than earning more money.

🧠 = Financial awareness

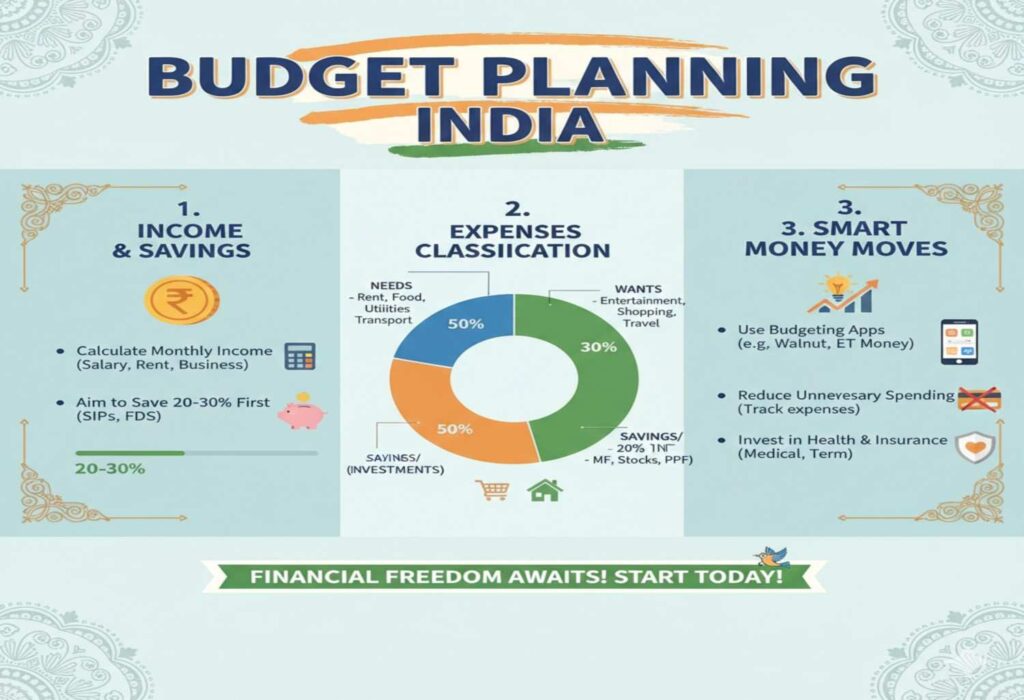

Step 1: Budgeting & Spending Wisely (Most Important Rule)

Budgeting means telling your money where to go, instead of wondering where it went.

✅ Simple Budget Rule for Indians: 50–30–20

| Category | Percentage | Example (₹40,000 income) |

| 🏠 Needs | 50% | ₹20,000 (rent, food, bills) |

| 🎉 Wants | 30% | ₹12,000 (shopping, OTT, travel) |

| 💾 Savings | 20% | ₹8,000 (SIP, emergency fund) |

👨👩👦 Real Life Example

Amit (30, Pune)

Amit used to save “whatever is left” at month-end — mostly nothing.

After following this rule, he automatically saves ₹8,000 every month without stress.

📊 = Control over money

Step 2: Emergency Savings Before Excessive Spending

Before buying:

- A new mobile 📱

- Bike or car 🚗

- Planning vacation ✈️

👉 Build an emergency fund first.

💡 What Is an Emergency Fund?

Money kept aside for:

- Medical emergencies

- Job loss

- Sudden family needs

📌 How Much Emergency Fund Is Enough?

👉 3–6 months of monthly expenses

Example:

Monthly expense = ₹25,000

Emergency fund target = ₹75,000 – ₹1,50,000

🛡️ = Financial safety net

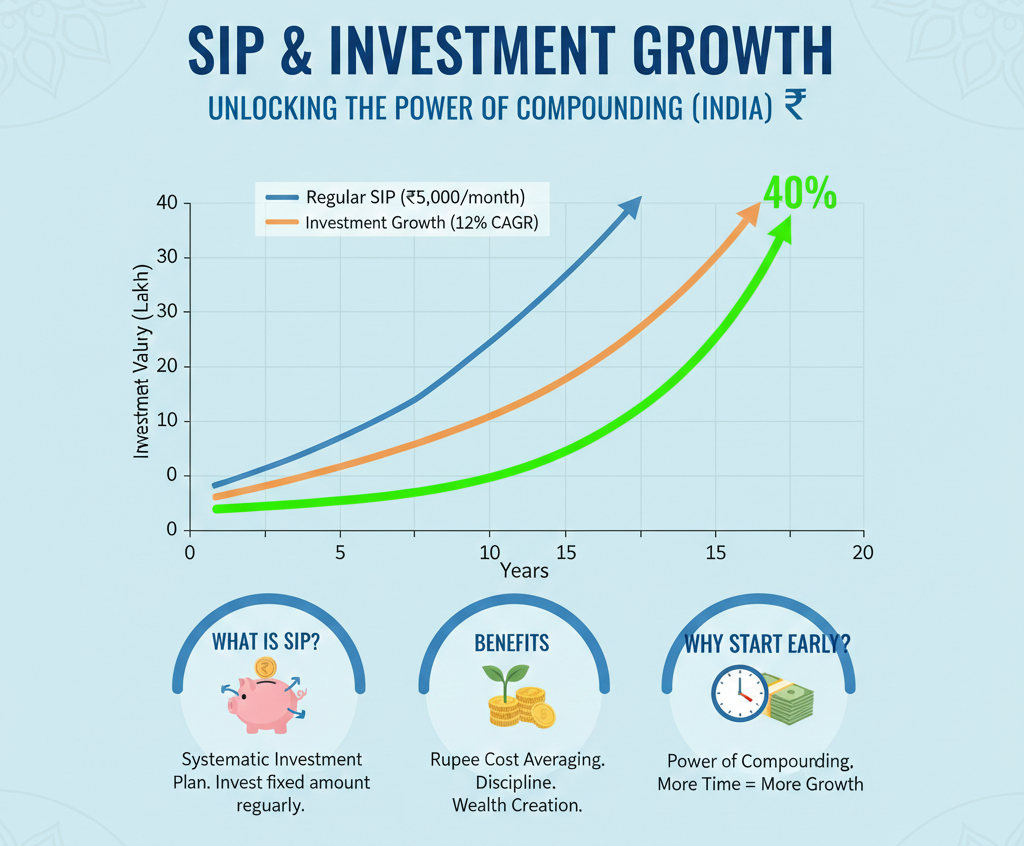

Step 3: Smart Investing Even with Small Money

In 2026, investing is no longer only for rich people.

✅ Best Investment Options for Beginners in India

- SIP (Systematic Investment Plan) – start from ₹500

- ETFs – low-cost and diversified

- Digital Gold – buy gold online in small quantity

👩 Real Life Example

Khushbu (25, Maharashtra)

Khushbu started SIP with just ₹1,000 per month.

After 3 years, she built a habit of investing and financial discipline.

🌱 = Small investment, big future

Step 4: Use Digital Finance Tools Smartly

India is leading the world in digital payments.

🔧 Useful Digital Tools

- UPI apps – track daily expenses

- Bank apps – auto savings & FD

- Google Sheets / expense apps – monthly budgeting

💡 Pro Tip:

Set auto-transfer for savings immediately after salary credit.

📱 = Technology + discipline

Common Money Mistakes People Should Avoid

❌ No budgeting

❌ No emergency fund

❌ Spending on credit cards without planning

❌ Emotional investing based on social media tips

Avoiding these mistakes can save you lakhs over time.

Simple Money Habits That Work in 2026

✔ Track expenses weekly

✔ Save first, spend later

✔ Increase SIP with salary hikes

✔ Avoid unnecessary loans

🔄 = Consistency builds wealth

Frequently Asked Questions (FAQ)

Is SIP safe for beginners?

👉 Yes. SIP is one of the best and safest ways to start investing.

Should I invest before creating an emergency fund?

👉 No. Emergency fund should come first.

Can low-income earners invest?

👉 Absolutely. Start with ₹500 SIP and grow gradually.

Are digital finance apps safe in India?

👉 Yes, if you use trusted apps and enable security features.