Introduction

A credit card limit increase is not a favor from your bank. It is a risk recalibration decision.

Under the regulatory supervision of the Reserve Bank of India, Indian banks must follow transparent billing and reporting norms — but credit limit decisions are governed by internal risk models.

And here’s the reality 👇

Limit enhancement approval depends on:

- Income trajectory

- Repayment discipline

- Credit bureau exposure

- Internal behavior scoring

- Macroeconomic risk environment

A higher limit can strengthen your credit profile.

But it can also amplify financial risk.

The objective is not to borrow more.

It is to optimize credit structure.

Executive Insight (Why This Matters in 2026)

In today’s Indian unsecured credit environment:

📈 Salaries are rising

📲 Digital spending is frictionless

🏦 Banks are tightening underwriting

📊 Loans are priced based on credit score

Your credit limit is part of your financial identity.

A disciplined borrower with optimized limits:

- Improves credit utilization ratio

- Enhances loan eligibility

- Strengthens long-term borrowing power

An undisciplined borrower:

- Increases unsecured exposure

- Weakens underwriting perception

- Pays higher lifetime interest

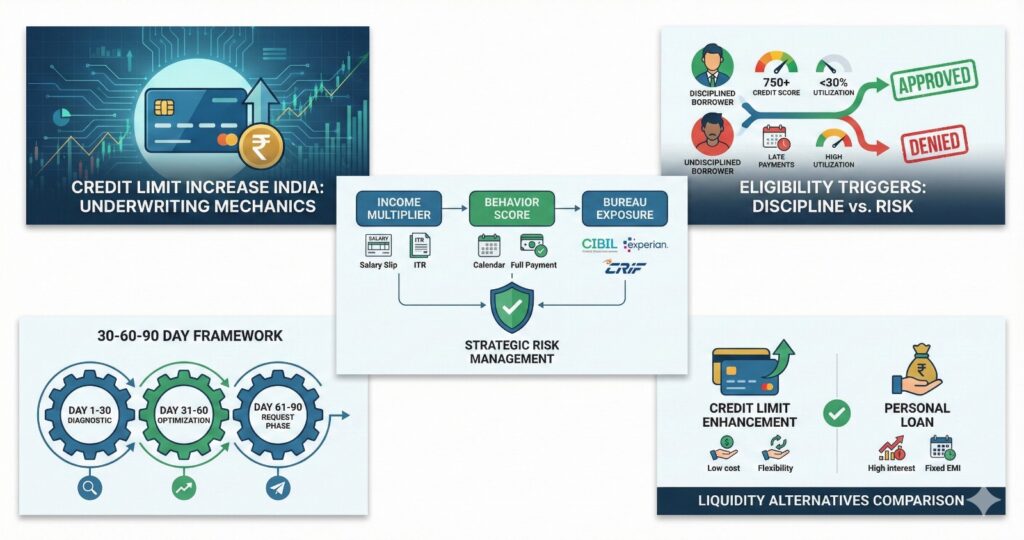

1️⃣ How Indian Banks Decide Credit Card Limits

Credit limit decisions are algorithmic.

While each bank uses proprietary scoring systems, the core underwriting pillars are consistent across India.

A. Income Multiplier Model

Most banks apply a multiplier on verifiable income.

Salaried Professionals

Typically: 2–4× monthly net salary

If your monthly take-home is ₹60,000 →

Potential range: ₹1.2 lakh – ₹2.4 lakh

Self-Employed Borrowers

Based on:

- 2–3 years Income Tax Returns

- Declared net income

- Profit consistency

Multipliers are generally more conservative due to income variability.

⚠️ If your income has increased but you haven’t updated documents, your limit may remain artificially low.

B. Internal Behaviour Score

Banks continuously track:

✔ Payment timeliness

✔ Full payment vs minimum due

✔ EMI conversions

✔ Revolving balance frequency

✔ Cash withdrawals

Consistent full repayments build internal credibility.

💡 Minimum due pattern reduces approval probability.

C. Bureau Exposure

Indian lenders pull data from:

- TransUnion CIBIL

- Experian

- CRIF High Mark

They evaluate:

- Total unsecured debt

- Recent credit inquiries

- Personal loans / BNPL exposure

- Credit utilization across cards

A score above 750 significantly improves approval probability.

D. Credit Utilization Ratio (CUR)

Formula:

CUR = (Outstanding ÷ Total Limit) × 100

Banks prefer:

- Below 30% → Excellent

- 30–40% → Acceptable

- Above 60% → Risk signal

Persistent high utilization indicates liquidity stress.

2️⃣ Why a Higher Limit Can Improve Your Credit Score

Scenario 1: No Enhancement

Limit: ₹1,00,000

Usage: ₹45,000

CUR = 45%

Moderate stress perception.

Scenario 2: Limit Increased to ₹2,00,000

Same usage: ₹45,000

CUR = 22.5%

Improved credit profile — without increasing spending.

🎯 Key Insight:

Limit increase improves score only if spending remains stable.

If spending rises proportionally, benefit disappears.

3️⃣ Early-Career Salaried Professionals (22–35 Years)

Typical Profile:

- 1–3 credit cards

- Growing salary

- Limited liabilities

Primary Approval Drivers

✔ Updated salary documentation

✔ Stable employer

✔ Zero late payments

✔ Low utilization

✔ No recent personal loans

Tactical Levers

📌 Submit increment letter or updated Form 16

📌 Reduce balance below 30% before request

📌 Maintain 6–9 months clean repayment history

📌 Avoid multiple parallel applications

Banks reward stability — not urgency.

4️⃣ Self-Employed Borrowers: Stricter Underwriting

Risk perception is higher due to income volatility.

What Banks Evaluate

- 2–3 years ITR

- Profit consistency

- Bank statement stability

- GST compliance

- Debt service ratio

Strategic Reality

Under-reporting income to save tax may reduce enhancement eligibility.

Declared profitability drives multiplier.

Mixing personal and business transactions reduces underwriting clarity.

Self-employed borrowers are typically assigned lower multipliers than salaried peers with similar gross income.

5️⃣ Liquidity Alternatives (Structural Comparison)

| Instrument | Cost Structure | Risk Level | Liquidity | Tax Treatment | Suitable For |

| Credit Limit Enhancement | Zero cost if unpaid balance cleared | Medium | High | No tax impact | Salaried professionals |

| Personal Loan | Fixed EMI + interest | High | High | Interest not deductible (personal use) | Short-term gap |

| FD-Backed Secured Card | Low | Low | Medium | FD interest taxable | New-to-credit |

| Business Overdraft | Variable interest | Medium | Medium | Deductible if business expense | Established self-employed |

💡 Enhancement is structurally cheaper than personal loan — if balance is paid in full.

6️⃣ Risk Analysis

A. Behavioural Escalation Risk

Higher limits can trigger:

❌ Lifestyle inflation

❌ Impulse purchases

❌ EMI stacking

Available credit increases consumption elasticity.

B. Home Loan Underwriting Impact

Banks calculate FOIR (Fixed Obligation to Income Ratio).

While unused limit does not increase EMI, large unsecured exposure may influence perception during major loan approval.

C. Economic Tightening Cycles

During downturns, banks may:

- Reduce limits

- Tighten underwriting

- Increase scrutiny

High limit is not a permanent entitlement.

7️⃣ Taxation Implications in India

✔ Limit enhancement has no tax implication

✔ Personal credit card interest is not deductible

✔ Business-use interest may be deductible if properly accounted

❌ Late fees and penalties are not deductible

8️⃣ Common Behavioural Mistakes

Salaried Professionals

- Applying to multiple banks simultaneously

- Converting discretionary expenses to EMIs

- Treating credit limit as income growth

Self-Employed Borrowers

- Suppressing taxable income

- Ignoring credit mix

- Using personal card for volatile business flow

9️⃣ 30–60–90 Day Strategic Framework

Days 1–30: Diagnostic

✔ Check credit report

✔ Calculate utilization

✔ Reduce balance below 30%

✔ Avoid new loan applications

Days 31–60: Optimization

✔ Update income with bank

✔ Maintain zero-late streak

✔ Avoid cash withdrawals

✔ Reduce EMI conversions

Days 61–90: Request Phase

✔ Apply via official bank channel

✔ Avoid parallel applications

✔ Monitor bureau score

✔ If rejected, wait 6 months

Discipline improves probability.

Strategic Interpretation: Credit Limit as Capital Structure Tool

A higher limit improves:

✔ Liquidity flexibility

✔ Utilization ratio

✔ Emergency capacity

But increases:

❌ Behavioural risk

❌ Unsecured exposure

❌ Underwriting scrutiny

Final Conclusion

Increasing your credit card limit in India is not about speed.

It is about alignment with underwriting mechanics.

Banks reward:

- Predictable income

- Disciplined repayment

- Low utilization

- Stable bureau exposure

For salaried professionals → salary growth + repayment discipline are key.

For self-employed borrowers → documented profitability matters more than headline income.

A higher limit can strengthen your financial structure.

It becomes damaging when treated as purchasing power expansion.

In India’s tightening unsecured credit environment, disciplined borrowers gain structural advantage.

The goal is not maximum credit.

It is optimized credit.

Frequently Asked Questions

Does increasing my credit card limit improve my CIBIL score?

Yes, if your spending remains the same and utilization drops. Higher limits improve your ratio only when balances stay controlled.

What credit score is required for a limit increase?

Most banks prefer a 750+ score for high approval probability. Lower scores may qualify but depend on income stability and repayment behavior.

Do banks automatically increase credit card limits?

Yes, banks may offer pre-approved increases based on internal behavior scoring and income trends. These usually have higher approval chances.

Can self-employed individuals increase their credit card limit?

Yes, but banks evaluate 2–3 years of ITRs, profit consistency, and banking stability more strictly than salaried applicants

What is the biggest mistake after getting a limit increase?

Increasing spending with the new limit. A higher limit should improve utilization, not fund lifestyle inflation.