💳 Credit cards are powerful financial tools — but only if you use them correctly.

In India, credit cards are regulated payment instruments, not long-term borrowing tools. Under the framework of the Reserve Bank of India, banks must follow structured billing, consent, and reporting rules.

But here’s the reality 👇

Regulation controls transparency — not interest rates.

Most Indian credit cards charge 30%–48% annual interest, compounded monthly.

For young professionals (22–30 years), early credit card habits shape your credit score with TransUnion CIBIL — and that directly affects your future home loan, car loan, and personal loan interest rates.

💡 A small mistake today can cost lakhs tomorrow.

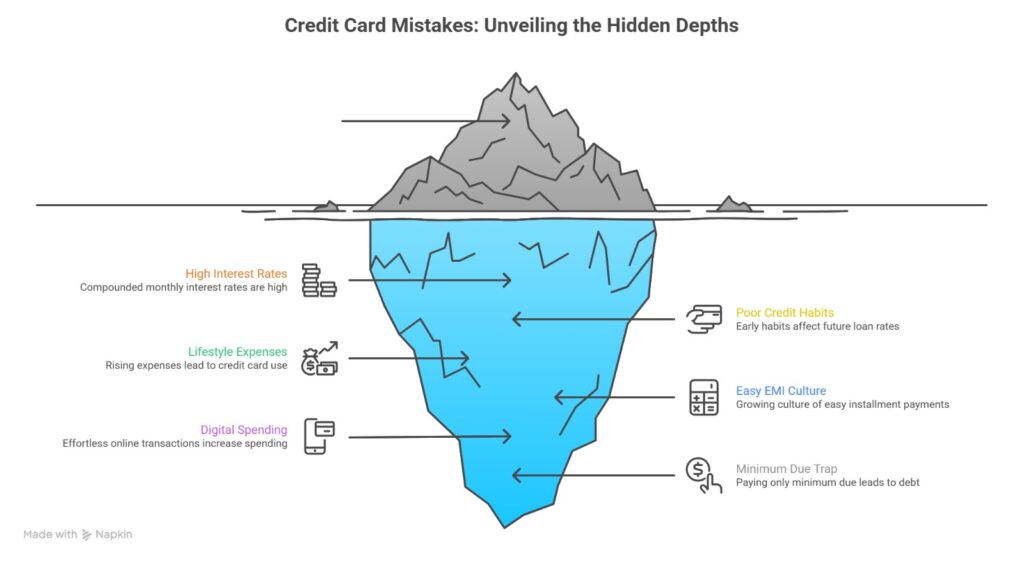

📌 Why Credit Card Discipline Matters in 2026

In today’s India:

- Lifestyle expenses are rising 📈

- Easy EMI culture is growing

- Digital spending makes swiping effortless

- Banks price loans based on credit score

👉 Your credit behavior in your 20s builds your financial identity.

Credit score range (CIBIL): 300–900

Higher score = Lower interest rates

Lower score = Higher lifetime borrowing cost

🧮 How Credit Cards Actually Work (Simple Explanation)

Credit cards operate on 5 key pillars:

1️⃣ Billing Cycle – ~30 days

2️⃣ Interest-Free Period – Up to 45–50 days (only if full payment is made)

3️⃣ Interest Rate – 30%–48% annually (2.5–4% per month)

4️⃣ Minimum Due – Usually ~5% of outstanding

5️⃣ Monthly Reporting to Credit Bureau

⚠️ Important: If you don’t pay full outstanding, the interest-free period disappears.

💸 The Minimum Due Trap (Why It’s Dangerous)

Example:

Outstanding: ₹50,000

APR: 42%

Monthly interest: 3.5%

Minimum due (5%) = ₹2,500

Month 1:

Interest = ₹50,000 × 3.5% = ₹1,750

Actual principal reduced = ₹750

You paid ₹2,500… but reduced only ₹750.

Effective Annual Cost

(1.035)¹² − 1 ≈ 51% effective annual interest

That means ₹50,000 debt can cost ₹20,000+ in interest in one year.

💣 Minimum due is not safety — it is slow compounding.

🚫 Major Credit Card Mistakes (With Real Impact)

1️⃣ Paying Only Minimum Due

Immediate effect:

✔ Avoid late fee

✔ No 30-day delay record

Long-term effect:

❌ Full interest charged

❌ Compounding starts

❌ Credit utilization remains high

Result over 2 years:

You may pay ₹70,000–₹80,000 for ₹50,000 usage.

2️⃣ High Credit Utilization

📌 Utilization = Outstanding ÷ Total Credit Limit

| Utilization | Meaning |

| Below 30% | Excellent |

| 30–50% | Acceptable |

| 50–75% | Risky |

| Above 75% | High Risk |

Example:

Limit: ₹1,00,000

Outstanding: ₹80,000

Utilization = 80%

Even if you pay on time, high utilization can reduce your score.

Long-Term Cost Example

Home loan: ₹50 lakh

Tenure: 20 years

At 8.5% → EMI ≈ ₹43,391

At 9.0% → EMI ≈ ₹44,986

Difference: ₹1,595 per month

Total extra payment ≈ ₹3.8 lakh

⚠️ Poor credit usage in your 20s can increase lifetime loan cost.

3️⃣ Missing Due Date

Under RBI norms:

3-day delay → Late fee

30+ days → Reported to bureau

90+ days → Loan classified stressed

One 30-day delay can:

- Drop score by 70–100 points

- Stay visible for years

- Increase loan rejection risk

📉 One missed payment can delay your financial goals.

4️⃣ Cash Withdrawals from Credit Card

Example: ₹20,000 withdrawal

Fee: 2.5–3% (~₹600)

GST: ~₹108

Immediate interest starts

Effective annual cost can exceed 45–50%.

Banks view cash withdrawal as liquidity stress signal.

🚨 Avoid unless extreme emergency.

5️⃣ Closing Your Oldest Card

Credit score depends on:

- Average credit age

- Oldest account history

Closing your oldest card can reduce score by 10–30 points.

If annual fee is the issue, downgrade instead of closing.

6️⃣ Multiple Card Applications

Each application creates a hard inquiry.

Many inquiries in 3–6 months:

- Signals credit hunger

- Reduces score temporarily

- Triggers underwriting caution

Avoid new applications before major loan.

📊 Mistake vs Financial Impact

| Mistake | Financial Cost | Credit Score Impact | Long-Term Effect |

| Minimum Due | ~51% effective interest | High | Lakhs in future loans |

| Utilization >75% | Indirect | Moderate–High | Higher loan rates |

| Late Payment | Late fee + interest | Severe | Loan rejection risk |

| Cash Advance | 45–50% cost | Moderate | Negative profile |

| Multiple Applications | None direct | Temporary | Scrutiny in loan approval |

💡 Behavioral Mistakes Young Professionals Make

❌ Treating credit limit as income

❌ Chasing reward points

❌ Assuming future salary will fix debt

❌ Taking too many EMIs

❌ Spending due to peer pressure

Remember:

2% cashback cannot offset 42% interest.

🛡️ Credit Discipline Framework (Simple System)

✅ Rule 1: Keep Utilization Below 30%

Limit ₹1,00,000 → Statement balance ≤ ₹30,000

✅ Rule 2: Auto-Debit Full Payment

Never auto-debit minimum due.

✅ Rule 3: Optimize Statement Date

Make big purchases just after statement generation.

✅ Rule 4: Two-Card Strategy

One primary card + one backup.

✅ Rule 5: Check Credit Report Annually

Look for:

- Errors

- Fraud

- Incorrect delays

✅ Rule 6: Clean Profile Before Major Loan

6 months before home/car loan:

- Reduce balances

- Avoid new applications

- Don’t close old cards

⚠️ Risks to Understand

Structural Risks:

- High unsecured interest rates

- Variable APR

- Data reporting errors

Personal Risks:

- Income instability

- Emotional spending

- Overconfidence in salary growth

Credit cards amplify financial behavior — good or bad.

🎯 Final Strategic Conclusion

Credit cards are:

✔ Short-term liquidity tools

✔ Credit score builders

✔ Financial discipline instruments

They are NOT:

❌ Income support

❌ Long-term loans

❌ Emergency substitutes

A 750 vs 820 credit score difference can change:

- Loan approval

- Interest spread

- Processing scrutiny

Over 20–25 years, disciplined usage can save several lakhs.

Frequently Asked Questions (FAQ)

Does paying only the minimum due affect my credit score?

It avoids late payment reporting, but high outstanding balances increase utilization, which can negatively impact your score over time.

What happens if I miss a credit card payment?

A delay beyond 30 days can be reported to credit bureaus, significantly reducing your credit score and affecting future loan approvals.

Are credit card cash withdrawals advisable?

No. They attract immediate interest and additional fees, making them one of the most expensive borrowing options.

Does applying for multiple credit cards reduce my score?

Yes, multiple applications within a short period create hard inquiries, which can temporarily lower your score.

What is the biggest credit card mistake young professionals make?

Treating the credit limit as income instead of a repayment obligation.