Many traders in India ask the same question:

“Is my stock or crypto profit treated as Capital Gains or Business Income?”

The answer is not based on one single rule.

It depends on intention, frequency, volume, and conduct of trading activity.

Understanding this classification is critical because taxation, compliance requirements, and even audit obligations change completely once trading is treated as business income.

If you actively trade shares, F&O, intraday, or crypto assets, this guide will help you understand when your activity crosses into business territory.

Capital Gains vs Business Income: Why Classification Matters

Under the Income Tax Act, trading profits can fall under two heads:

- Capital Gains

- Profits and Gains from Business or Profession

The tax rate, loss adjustment rules, audit applicability, and compliance requirements differ significantly between the two.

For example:

- Capital Gains may attract concessional rates (depending on asset type).

- Business Income is taxed at slab rates and may require maintenance of books and tax audit.

So classification is not just technical — it affects your real tax liability.

When Is Stock Trading Treated as Business Income?

There is no fixed numerical threshold under Indian tax law.

Instead, tax authorities evaluate the nature of activity.

Stock trading is generally treated as Business Income when:

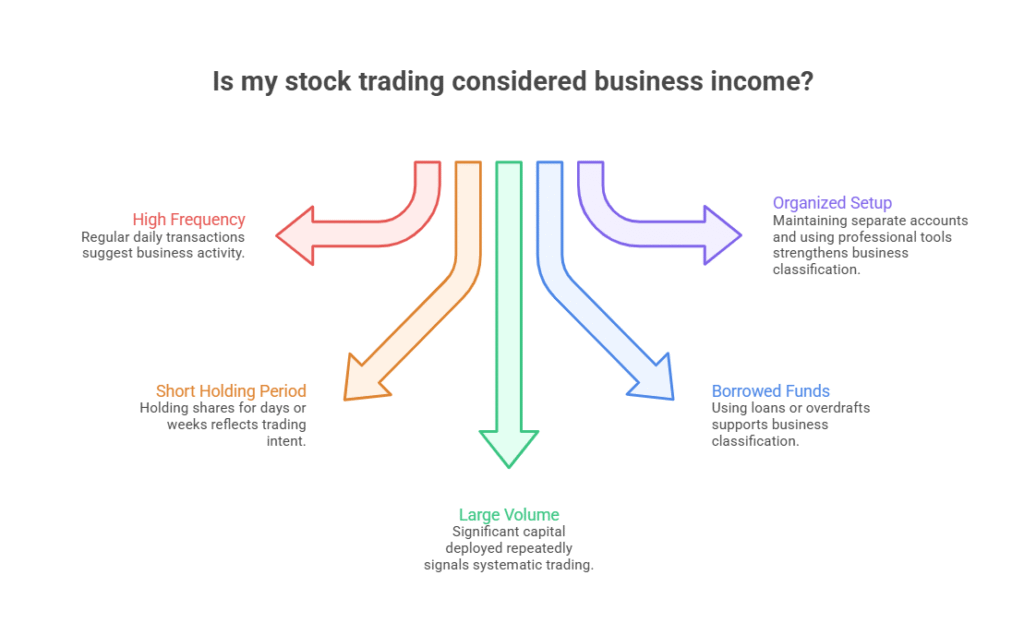

1. High Frequency of Transactions

Buying and selling shares regularly, almost daily, indicates business activity rather than investment.

2. Short Holding Period

If shares are held for very short durations (days or weeks), it reflects trading intent.

3. Large Volume and Turnover

Significant capital deployed repeatedly in the market may signal systematic trading.

4. Use of Borrowed Funds

If you use loans or overdrafts to trade, it supports business classification.

5. Organized Setup

Maintaining separate trading accounts, using professional tools, or showing trading as primary income source strengthens business classification.

Special Case: Intraday and F&O Trading

Intraday equity trading and Futures & Options are typically treated as business income in India.

- Intraday trading → Speculative business income

- F&O trading → Non-speculative business income

In most cases, these are not treated as capital gains.

When Does Crypto Trading Become Business Income?

Crypto taxation in India operates under special provisions.

However, classification still depends on activity pattern.

Crypto trading may be treated as business income when:

- There is frequent buying and selling of virtual digital assets.

- Activity resembles organized trading rather than passive holding.

- Income is regular and substantial.

- Trading is primary source of livelihood.

If crypto is held occasionally as investment and sold after a long holding period, the treatment may differ.

But once trading becomes systematic and repetitive, it leans toward business characterization.

Key Factors Tax Authorities Consider

The Income Tax Department generally evaluates:

- Intention at the time of purchase

- Frequency and regularity of transactions

- Volume and magnitude

- Time devoted to trading activity

- Source of funds

- Overall conduct of taxpayer

No single factor is decisive.

It is the cumulative pattern that determines classification.

What Happens If Trading Is Treated as Business Income?

If your stock or crypto activity is classified as business income:

You may need to:

- Maintain books of accounts

- Compute turnover correctly (especially in F&O)

- Pay advance tax

- Consider tax audit applicability if turnover exceeds prescribed limits

- File ITR under business head

Tax rates will apply as per individual slab rates.

Loss treatment rules will also change compared to capital gains.

Why Misclassification Can Be Risky

Incorrectly reporting active trading as capital gains can:

- Trigger tax scrutiny

- Lead to reclassification

- Attract penalty and interest

On the other hand, declaring genuine investments as business income may unnecessarily increase compliance burden.

Proper classification reduces litigation risk.

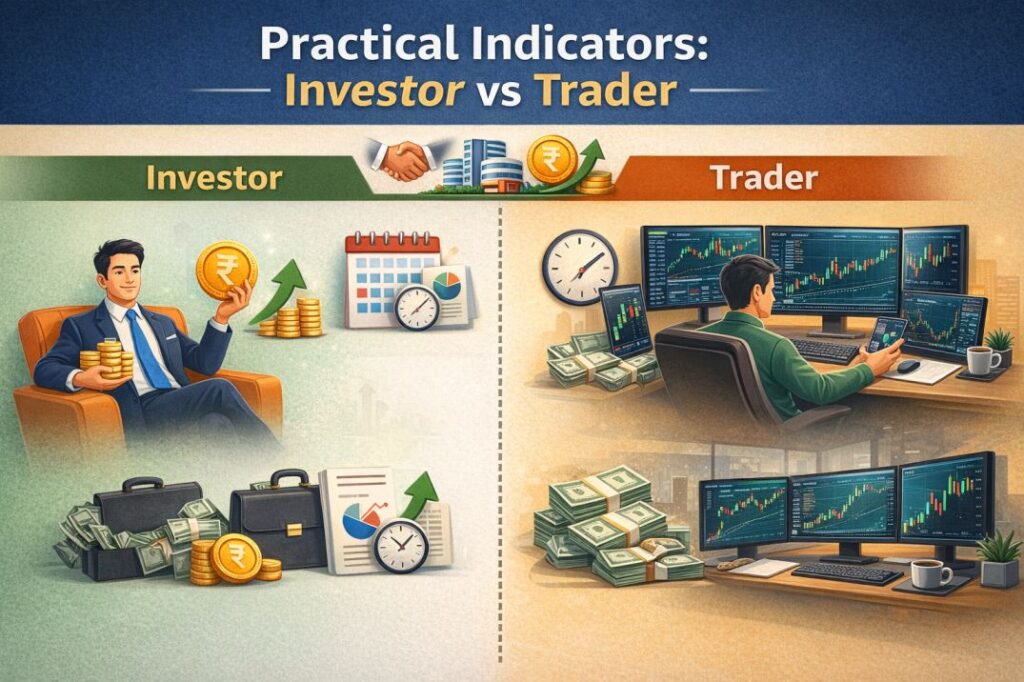

Practical Indicators: Investor vs Trader

You are more likely an investor if:

- You buy and hold for long term.

- Transactions are limited.

- Trading is not your primary income source.

You are more likely a trader if:

- You transact frequently.

- Short holding periods dominate.

- Trading income forms major part of earnings.

- Activity is systematic and organized.

Does Turnover Alone Decide?

Answer is No.

There is no fixed turnover limit that automatically converts trading into business income.

However, high turnover combined with frequency and systematic activity strongly indicates business nature.

Final Takeaway

Stock or crypto trading becomes business income in India when the activity is:

- Frequent

- Systematic

- Organized

- Profit-driven with trading intent

The classification depends on behavior, not just profit amount.

If your activity resembles a commercial operation rather than passive investment, it is likely to be treated as business income.

Correct classification ensures:

- Proper tax reporting

- Compliance safety

- Reduced litigation risk

Before filing your return, always evaluate your trading pattern carefully.

Because in taxation, intent and conduct matter more than labels.

SUGGESTED LINKS

Taxation of Virtual Digital Assets (VDA) in India

TCS on Car Purchase – How to Claim TCS Refund on Car Purchase?

Different Types of Income Tax Notices & Their Time Limits (India)

Is intraday or F&O trading always treated as business income?

In practice, yes.

Intraday equity trading is generally treated as speculative business income.

Futures and Options (F&O) trading is treated as non-speculative business income.

Such transactions are not typically assessed under capital gains because they involve trading without delivery and are considered commercial activities in nature.

Can crypto trading be reported as capital gains instead of business income?

It depends on the pattern of activity.

If crypto is purchased as an investment and sold occasionally, capital gains characterization may be supportable.

However, frequent and systematic trading of virtual digital assets may indicate business activity.

The determining factors include:

Volume of trades

Frequency

Source of funds

Whether trading is primary income source

The tax department evaluates substance over form.

Does high turnover automatically mean trading is business income?

No, turnover alone is not decisive.

However, high turnover combined with:

Short holding cycles

Repetitive buying and selling

Organized trading conduct

May strongly indicate business intent.

Turnover is a relevant factor, but it must be evaluated alongside behavioral and operational indicators.

What are the compliance implications if trading is classified as business income?

If trading income is treated as business income, the taxpayer may be required to:

Maintain books of accounts

Compute turnover accurately (especially in derivatives)

Pay advance tax

Evaluate tax audit applicability

File return under business head

Failure to comply with these requirements may lead to interest, penalties, or scrutiny.

Correct classification ensures tax sustainability and reduces litigation risk.